Social Security Update

Social Security and Medicare Taxes

Social Security's Old-Age, Survivors, and Disability Insurance (OASDI) program limits the amount of earnings subject to taxation for a given year. The same annual limit also applies when those earnings are used in a benefit computation. This limit changes each year with changes in the national average wage index. We call this annual limit the contribution and benefit base. This amount is also commonly referred to as the taxable maximum. For earnings in 2024, this base is $168,600 and $176,100 for 2025.

The OASDI tax rate for wages paid in 2024 is set by statute at 6.2 percent for employees and employers, each. Thus, an individual with wages equal to or larger than $168,600 would contribute $10,453.20 to the OASDI program in 2024, and his or her employer would contribute the same amount. The OASDI tax rate for self-employment income in 2024 is 12.4 percent. The FICA maximum for 2025 is $176,100, which is the Social Security wage base. This is an increase from $168,600 in 2024. The FICA tax rate for 2025 is 7.65%, which is made up of 6.2% for Social Security and 1.45% for Medicare. The Social Security tax rate for employees and employers is 6.2%, while the self-employed pay 12.4%.

For Medicare's Hospital Insurance (HI) program, the taxable maximum was the same as that for the OASDI program for 1966-1990. Separate HI taxable maximums of $125,000, $130,200, and $135,000 were applicable in 1991-93, respectively. After 1993, there has been no limitation on HI-taxable earnings. Tax rates under the HI program are 1.45 percent for employees and employers, each, and 2.90 percent for self-employed persons.

Social Security's Old-Age, Survivors, and Disability Insurance (OASDI) program limits the amount of earnings subject to taxation for a given year. The same annual limit also applies when those earnings are used in a benefit computation. This limit changes each year with changes in the national average wage index. We call this annual limit the contribution and benefit base. This amount is also commonly referred to as the taxable maximum. For earnings in 2024, this base is $168,600 and $176,100 for 2025.

The OASDI tax rate for wages paid in 2024 is set by statute at 6.2 percent for employees and employers, each. Thus, an individual with wages equal to or larger than $168,600 would contribute $10,453.20 to the OASDI program in 2024, and his or her employer would contribute the same amount. The OASDI tax rate for self-employment income in 2024 is 12.4 percent. The FICA maximum for 2025 is $176,100, which is the Social Security wage base. This is an increase from $168,600 in 2024. The FICA tax rate for 2025 is 7.65%, which is made up of 6.2% for Social Security and 1.45% for Medicare. The Social Security tax rate for employees and employers is 6.2%, while the self-employed pay 12.4%.

For Medicare's Hospital Insurance (HI) program, the taxable maximum was the same as that for the OASDI program for 1966-1990. Separate HI taxable maximums of $125,000, $130,200, and $135,000 were applicable in 1991-93, respectively. After 1993, there has been no limitation on HI-taxable earnings. Tax rates under the HI program are 1.45 percent for employees and employers, each, and 2.90 percent for self-employed persons.

Contribution and benefit bases, 1937-2025

Note: Amounts fro 1937-74 and for 1979-8 were set by statute; all other amounts were determined under automatic adjustment provisions of the Social Security Act.

For more information on Social Security and Medicare Contribution and Benefit Base, please go here

Retirement Benefits

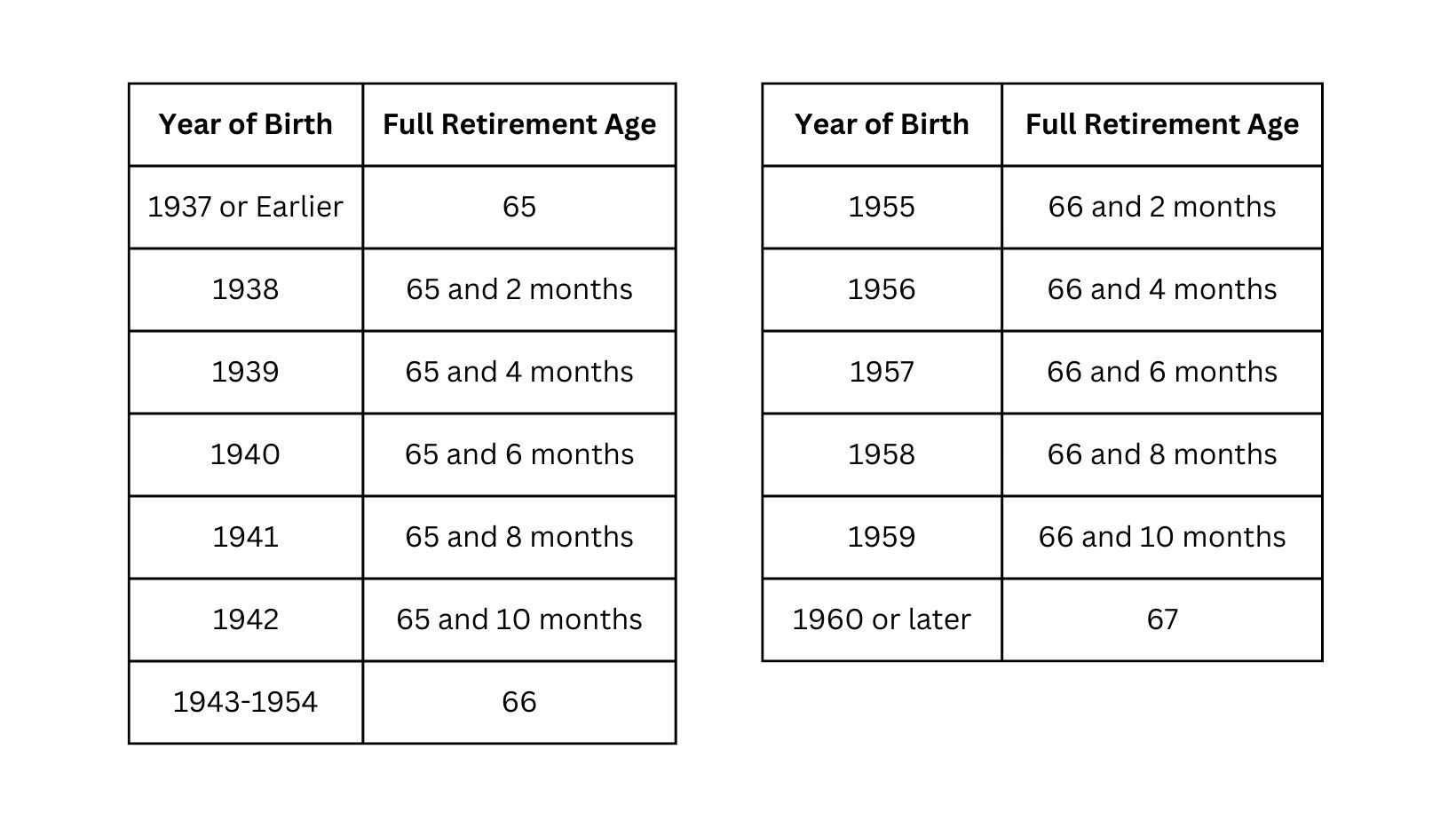

Under the present tax law, you are eligible for full benefits at age 65. If you were born after 1937, the age at which you can receive full benefits rises. In addition, most individuals must have accumulated 10 years or 40 quarters of earnings experience to obtain full retirement benefits from social security. In 2024, to earn a quarter of experience you must earn at least $900 during that quarter. The maximum number of quarters you can per year is four.

Under the present tax law, you are eligible for full benefits at age 65. If you were born after 1937, the age at which you can receive full benefits rises. In addition, most individuals must have accumulated 10 years or 40 quarters of earnings experience to obtain full retirement benefits from social security. In 2024, to earn a quarter of experience you must earn at least $900 during that quarter. The maximum number of quarters you can per year is four.

You can delay taking your benefits until age 70. If your yearly earnings are higher than your past average earnings then you will qualify for higher benefits when you retire. This is because the highest paying yearly earnings are taken into consideration when determining your benefit at retirement.

You may start receiving benefits as early as age 62. In 2024, your benefits would be permanently reduced by 5/9 of 1 percent for each month before your full retirement age. Thus, if you retire at age 62 in 2024 your benefits would be reduced by 23.33%. The breakeven point is 15 years. Thus at age 77 you would receive more gross full retirement benefits than retiring early at 62 and receiving only partial retirement benefits.

The reduction percentage will be greater in future years as the full retirement age increases. The choice is whether to retire early and receive lesser benefits for a longer period of time or retire later and receive greater benefits per month.

If you continue working while receiving benefits, then your benefits may be reduced if you exceed the earnings limit for that year. The earnings limits for 2024 are noted below:• Non-blind individuals-- $970 per month• Blind individuals-- $1,340 per month• Individuals under Age 65-- for every $2 over $11,640 ($970 per month), $1 is withheld from benefits.• Year individual reaches retirement age 65-- for every $3 over $31,080 ($2,590/mo), $1 is withheld from benefits (applies only to earnings before the month you reach full retirement age).• Individuals age 65 or older-- no limit on earnings (starting with the month you reach Full Retirement Age). At age 70, it would be beneficial to apply for retirement benefits (if you have not already) even if you will be fully employed. Further, if you previously applied for Medicare the Social Security office logs in your date of birth and sends the first retirement check five years later, on your 70th birthday, even if you have not applied for retirement benefits.

A special monthly rule applies to your first year of retirement. If you retire mid-year (i.e., not on December 31) you can receive a full retirement benefit check for any month you are retired, regardless of your yearly earnings. Thus your monthly retirement benefits will be determined based on your monthly earnings. For example, if you are under 65 in year 2024 your monthly earning limit is $970 per month. Therefore, any month in which you earn $972, one dollar in benefit will be withheld for every $2 in earnings above the earnings limit.

For self-employed individuals, Social Security considers whether you perform substantial services in your business. In general, if you are self-employed more than 45 hours a month you are not considered retired. If you work less than 15 hours a month, you are considered retired. Between 15 and 45 hours a month, you are not considered retired if you work in an occupation that requires a lot of skill or if you manage a sizeable business.

If you sign up for Medicare benefits but not for retirement benefits, the Social Security Administration may take the position that you retired in the year you applied for Medicare. If you subsequently retire mid-year, the special monthly rule will not apply. In this case, it may be wise to take your retirement at the end of the year, or at least before you earn enough to have your benefits reduced. Please contact the office for additional information and assistance.

Family/Survivor Benefits

Some of the Social Security taxes you pay go towards survivors insurance. When someone who has worked and paid into Social Security dies, survivor benefits can be paid to certain family members. These members include widows, widowers (and divorced widows and widowers), children and dependent parents.

The number of credits you need for your family to qualify for survivor benefits depends on your age when you die. However, if you have earned credits for one and one-half years in the three years before your death (six credits), your family may qualify even though you do not have the number of credits needed.

There is a special one-time payment of $255 that can be made when you die if you have enough work "credits." This payment can be made only to your spouse or minor children if they meet certain requirements.

How much your family can get from Social Security depends on your average lifetime earnings. That means the higher your earnings, the higher their benefits will be. If you would like to get an estimate for the Social Security survivors benefits that could be paid to your family please contact our office.

Benefits taxable

This is a general overview on the taxation of your benefits. The calculations are very complicated and we strongly advise that you contact us to determine the taxability of your benefits.

If the only income you received during 2024 is your Social Security benefit, your benefits are unlikely to be taxed and you probably will not have to file a return.

However if you received other income, your benefits will not be taxed unless your modified adjusted gross income is more than the base amount for your filing status. Your modified adjusted gross income is computed by adding one-half of your Social Security benefits to all your other income, including any tax-exempt interest or exclusions from income. For tax year 2023, compare this total to your base amount:• $25,000 if you are single, head of household, or qualifying widow or widower with a dependent child;• $25,000 if you are married filing separately and did not live with your spouse at any time during the year;• $32,000 if you are married and file a joint return;• $0 if you are married filing separately and lived with your spouse at any time during the year. If your income is more than your base amount, part of your benefits will be taxable. The taxable amount of your benefits is computed on a worksheet in Form 1040 or 1040A instruction book.

The taxable benefits, if any, must be included in the gross income of the person who has the legal right to receive them. For example, if you and your child received benefits, but the check for your child was made out in your name, you must use only your own portion of the benefits in figuring if any part is taxable to you. The portion of the benefits that belong to your child must be added to your child's other income to see if any of those benefits are taxable.

If you are married and file a joint return, you and your spouse must combine your incomes and your Social Security benefits when figuring the taxable portion of your benefits.

If part of your benefits is taxable, enter both the total amount and the taxable amount of the benefits received on Form 1040 or 1040A. You cannot use Form 1040EZ.

You should receive your 2024 Form SSA-1099 by January 31, 2025. The form will show benefits paid to the person who has the legal right to get them, and the amount of any benefits you repaid in 2024. It will also show amounts by which the benefits were reduced because you received workers compensation benefits.

You may want to refer to the Internal Revenue Service Publication 915, "Social Security and Equivalent Railroad Retirement Benefits-- Are Any of Your Benefits Taxable?"

You may also be able to take a credit for being elderly or disabled. Generally, if you are age 65 or older or disabled and your income and nontaxable social security or other nontaxable pension are below specified amounts, you may be able to take this credit.

**Please contact our office for assistance and more details**

Supplemental Security Income (SSI)

SSI is a public assistance program that is not funded via our Social Security system but rather through general tax revenues. It is designed to ensure that certain individuals receive a minimum level of income. SSI pays monthly checks to individuals with the following requirements:

1. US citizen or legal permanent resident residing in the US or Northern Mariana Islands2. Earn minimal income3. At least 65 years or older, blind OR disabled AND

The basic SSI payment is the same nationwide. However, many states supplement the SSI payment with their own payment which varies from state to state.

The amount of payment also depends on how much you earn and own. Income that is not counted for determining eligibility includes:• the first $20 of most income received in a month;• the first $65 a month you earn from working and half the amount over $65;• food stamps;• shelter you get from private nonprofit organizations; and• most home energy assistance For students some of your wages or scholarships you receive may also not count.

For working and disabled individuals, Social Security does not count any wages you use to pay for items or services you need to work because of your disability. For example, if you need a wheelchair, the wages you use to pay for the wheelchair will not count as income. Or if some of the income you use or save for training may also not count as income.

Also, Social Security does not count any wages a blind person uses to pay expenses that are caused by working. For example, if a blind person uses wages to pay for transportation to and from work, the transportation cost isn't counted as income.

Your personal assets also determine your eligibility for SSI benefits. Items considered include real estate, personal belongings, bank accounts, cash and investments. Generally, a person with assets up to $2,000 can qualify for SSI. A couple may have up to $3,000 in assets.

Items that are excluded when determining SSI eligibility include:• Your personal residence• Life insurance policies with less than $1,500 face value• Your car• Burial plots for you and your immediate family• Up to $1,500 in burial funds for you and an additional $1,500 for your spouse• For the disabled, items you plan to use to work or earn extra income If you are eligible for Social Security or other benefits you must apply for them. You can receive both SSI and Social Security payments if you qualify for both.

Please contact our office for assistance and additional details.

Disability Benefits

The disability benefits program is one of the most complicated programs that is offered by Social Security.

To qualify for disability from Social Security, you must have a physical or mental impairment that is expected to keep you from doing any "substantial" work for at least a year (generally, average monthly earnings of $800 or more is considered substantial), or you must have a condition that is expected to result in your death. There are no payments for partial or short-term disabilities.

The monthly benefit payments begin with the sixth full month of disability. You will receive your first payment after this sixth month (e.g., disabled in June, benefits begin in December, first check in January). You need to apply for benefits as soon as you realize you're disabled or risk having your payments delayed beyond the six-month waiting period while your paperwork is processed.

If your condition improves or you begin "substantial" work, your benefits will cease. There are, however, special incentives to return to work rules which allow you to try working without a sudden loss of your monthly benefits.

Please contact our off for assistance and additional details.

Medicare

The Health Care Financing Administration (HCFA) administers Medicare, which is part of the Department of Health and Human Services. Medicare provides health insurance to individuals who fulfill one of the following:• Aged 65 and over,• Has a permanent kidney failure, or• Disabled prior to age 65 and entitled to Social security benefits for at least two years Medicare is divided in two parts. One part is the hospital insurance which is paid by a portion of your Social Security taxes. The second part is medical insurance which is paid partly by monthly premiums you must pay, and partly from general revenues from the government.

You can apply for benefits at any Social Security office. It is best to call ahead at 1-800-772-1213 to make an appointment. Please contact our office if we can be of any assistance in this area in regards to tax information.

Depending on which benefits you are applying for, the documents you'll need to bring will vary. All documents you bring must be originals or certified copies. Social Security will photocopy them and return the originals to you. A partial list of necessary documents include:• Your Social Security card (or a record of your number)• Your birth certificate• Proof of U.S. citizenship or lawful alien status if you were not born in the U.S.•Your spouse's birth certificate and Social Security number if he or she is applying for benefits based on your record• Marriage certificate if signing up on spouse's record• Your military discharge papers if you served in the military• Your most recent W-2, or a copy of your most recent tax return if you are self-employed• Your checkbook or account statement if you want to receive your benefits through direct deposit If you are applying for disability benefits, you will need to additionally provide the following:• Medical records from your doctors, therapists, hospitals, clinics, etc.• Your laboratory and test results• The names, addresses, phone numbers and fax numbers of your doctors, clinics and hospitals• The names of all medications you are taking• The names of your employers and your job duties for the last 15 years.

The reduction percentage will be greater in future years as the full retirement age increases. The choice is whether to retire early and receive lesser benefits for a longer period of time or retire later and receive greater benefits per month.

If you continue working while receiving benefits, then your benefits may be reduced if you exceed the earnings limit for that year. The earnings limits for 2024 are noted below:• Non-blind individuals-- $970 per month• Blind individuals-- $1,340 per month• Individuals under Age 65-- for every $2 over $11,640 ($970 per month), $1 is withheld from benefits.• Year individual reaches retirement age 65-- for every $3 over $31,080 ($2,590/mo), $1 is withheld from benefits (applies only to earnings before the month you reach full retirement age).• Individuals age 65 or older-- no limit on earnings (starting with the month you reach Full Retirement Age). At age 70, it would be beneficial to apply for retirement benefits (if you have not already) even if you will be fully employed. Further, if you previously applied for Medicare the Social Security office logs in your date of birth and sends the first retirement check five years later, on your 70th birthday, even if you have not applied for retirement benefits.

A special monthly rule applies to your first year of retirement. If you retire mid-year (i.e., not on December 31) you can receive a full retirement benefit check for any month you are retired, regardless of your yearly earnings. Thus your monthly retirement benefits will be determined based on your monthly earnings. For example, if you are under 65 in year 2024 your monthly earning limit is $970 per month. Therefore, any month in which you earn $972, one dollar in benefit will be withheld for every $2 in earnings above the earnings limit.

For self-employed individuals, Social Security considers whether you perform substantial services in your business. In general, if you are self-employed more than 45 hours a month you are not considered retired. If you work less than 15 hours a month, you are considered retired. Between 15 and 45 hours a month, you are not considered retired if you work in an occupation that requires a lot of skill or if you manage a sizeable business.

If you sign up for Medicare benefits but not for retirement benefits, the Social Security Administration may take the position that you retired in the year you applied for Medicare. If you subsequently retire mid-year, the special monthly rule will not apply. In this case, it may be wise to take your retirement at the end of the year, or at least before you earn enough to have your benefits reduced. Please contact the office for additional information and assistance.

Family/Survivor Benefits

Some of the Social Security taxes you pay go towards survivors insurance. When someone who has worked and paid into Social Security dies, survivor benefits can be paid to certain family members. These members include widows, widowers (and divorced widows and widowers), children and dependent parents.

The number of credits you need for your family to qualify for survivor benefits depends on your age when you die. However, if you have earned credits for one and one-half years in the three years before your death (six credits), your family may qualify even though you do not have the number of credits needed.

There is a special one-time payment of $255 that can be made when you die if you have enough work "credits." This payment can be made only to your spouse or minor children if they meet certain requirements.

How much your family can get from Social Security depends on your average lifetime earnings. That means the higher your earnings, the higher their benefits will be. If you would like to get an estimate for the Social Security survivors benefits that could be paid to your family please contact our office.

Benefits taxable

This is a general overview on the taxation of your benefits. The calculations are very complicated and we strongly advise that you contact us to determine the taxability of your benefits.

If the only income you received during 2024 is your Social Security benefit, your benefits are unlikely to be taxed and you probably will not have to file a return.

However if you received other income, your benefits will not be taxed unless your modified adjusted gross income is more than the base amount for your filing status. Your modified adjusted gross income is computed by adding one-half of your Social Security benefits to all your other income, including any tax-exempt interest or exclusions from income. For tax year 2023, compare this total to your base amount:• $25,000 if you are single, head of household, or qualifying widow or widower with a dependent child;• $25,000 if you are married filing separately and did not live with your spouse at any time during the year;• $32,000 if you are married and file a joint return;• $0 if you are married filing separately and lived with your spouse at any time during the year. If your income is more than your base amount, part of your benefits will be taxable. The taxable amount of your benefits is computed on a worksheet in Form 1040 or 1040A instruction book.

The taxable benefits, if any, must be included in the gross income of the person who has the legal right to receive them. For example, if you and your child received benefits, but the check for your child was made out in your name, you must use only your own portion of the benefits in figuring if any part is taxable to you. The portion of the benefits that belong to your child must be added to your child's other income to see if any of those benefits are taxable.

If you are married and file a joint return, you and your spouse must combine your incomes and your Social Security benefits when figuring the taxable portion of your benefits.

If part of your benefits is taxable, enter both the total amount and the taxable amount of the benefits received on Form 1040 or 1040A. You cannot use Form 1040EZ.

You should receive your 2024 Form SSA-1099 by January 31, 2025. The form will show benefits paid to the person who has the legal right to get them, and the amount of any benefits you repaid in 2024. It will also show amounts by which the benefits were reduced because you received workers compensation benefits.

You may want to refer to the Internal Revenue Service Publication 915, "Social Security and Equivalent Railroad Retirement Benefits-- Are Any of Your Benefits Taxable?"

You may also be able to take a credit for being elderly or disabled. Generally, if you are age 65 or older or disabled and your income and nontaxable social security or other nontaxable pension are below specified amounts, you may be able to take this credit.

**Please contact our office for assistance and more details**

Supplemental Security Income (SSI)

SSI is a public assistance program that is not funded via our Social Security system but rather through general tax revenues. It is designed to ensure that certain individuals receive a minimum level of income. SSI pays monthly checks to individuals with the following requirements:

1. US citizen or legal permanent resident residing in the US or Northern Mariana Islands2. Earn minimal income3. At least 65 years or older, blind OR disabled AND

The basic SSI payment is the same nationwide. However, many states supplement the SSI payment with their own payment which varies from state to state.

The amount of payment also depends on how much you earn and own. Income that is not counted for determining eligibility includes:• the first $20 of most income received in a month;• the first $65 a month you earn from working and half the amount over $65;• food stamps;• shelter you get from private nonprofit organizations; and• most home energy assistance For students some of your wages or scholarships you receive may also not count.

For working and disabled individuals, Social Security does not count any wages you use to pay for items or services you need to work because of your disability. For example, if you need a wheelchair, the wages you use to pay for the wheelchair will not count as income. Or if some of the income you use or save for training may also not count as income.

Also, Social Security does not count any wages a blind person uses to pay expenses that are caused by working. For example, if a blind person uses wages to pay for transportation to and from work, the transportation cost isn't counted as income.

Your personal assets also determine your eligibility for SSI benefits. Items considered include real estate, personal belongings, bank accounts, cash and investments. Generally, a person with assets up to $2,000 can qualify for SSI. A couple may have up to $3,000 in assets.

Items that are excluded when determining SSI eligibility include:• Your personal residence• Life insurance policies with less than $1,500 face value• Your car• Burial plots for you and your immediate family• Up to $1,500 in burial funds for you and an additional $1,500 for your spouse• For the disabled, items you plan to use to work or earn extra income If you are eligible for Social Security or other benefits you must apply for them. You can receive both SSI and Social Security payments if you qualify for both.

Please contact our office for assistance and additional details.

Disability Benefits

The disability benefits program is one of the most complicated programs that is offered by Social Security.

To qualify for disability from Social Security, you must have a physical or mental impairment that is expected to keep you from doing any "substantial" work for at least a year (generally, average monthly earnings of $800 or more is considered substantial), or you must have a condition that is expected to result in your death. There are no payments for partial or short-term disabilities.

The monthly benefit payments begin with the sixth full month of disability. You will receive your first payment after this sixth month (e.g., disabled in June, benefits begin in December, first check in January). You need to apply for benefits as soon as you realize you're disabled or risk having your payments delayed beyond the six-month waiting period while your paperwork is processed.

If your condition improves or you begin "substantial" work, your benefits will cease. There are, however, special incentives to return to work rules which allow you to try working without a sudden loss of your monthly benefits.

Please contact our off for assistance and additional details.

Medicare

The Health Care Financing Administration (HCFA) administers Medicare, which is part of the Department of Health and Human Services. Medicare provides health insurance to individuals who fulfill one of the following:• Aged 65 and over,• Has a permanent kidney failure, or• Disabled prior to age 65 and entitled to Social security benefits for at least two years Medicare is divided in two parts. One part is the hospital insurance which is paid by a portion of your Social Security taxes. The second part is medical insurance which is paid partly by monthly premiums you must pay, and partly from general revenues from the government.

You can apply for benefits at any Social Security office. It is best to call ahead at 1-800-772-1213 to make an appointment. Please contact our office if we can be of any assistance in this area in regards to tax information.

Depending on which benefits you are applying for, the documents you'll need to bring will vary. All documents you bring must be originals or certified copies. Social Security will photocopy them and return the originals to you. A partial list of necessary documents include:• Your Social Security card (or a record of your number)• Your birth certificate• Proof of U.S. citizenship or lawful alien status if you were not born in the U.S.•Your spouse's birth certificate and Social Security number if he or she is applying for benefits based on your record• Marriage certificate if signing up on spouse's record• Your military discharge papers if you served in the military• Your most recent W-2, or a copy of your most recent tax return if you are self-employed• Your checkbook or account statement if you want to receive your benefits through direct deposit If you are applying for disability benefits, you will need to additionally provide the following:• Medical records from your doctors, therapists, hospitals, clinics, etc.• Your laboratory and test results• The names, addresses, phone numbers and fax numbers of your doctors, clinics and hospitals• The names of all medications you are taking• The names of your employers and your job duties for the last 15 years.

There are other tax-cutting strategies in addition to those mentioned here. If you would like assistance in selecting tax-saving strategies that make the most sense in your situation, contact us today!